When families start looking into senior care, one of the first questions is always about the cost. It’s the elephant in the room, and figuring out the financial side is the first real step toward making a decision you feel good about.

In-home care is usually priced by the hour. That flexibility is great, but it can get expensive fast, especially for seniors who need consistent, round-the-clock support.

Think of it like hiring any professional for their time. You pay for a caregiver to be there, whether it's for a couple of hours a day to help with meals and medication reminders or for 24/7 supervision. For someone needing just a little help, it's a perfect fit. But as care needs grow, so do the costs, sometimes even surpassing other senior living options.

National and Texas Cost Averages

Let's get down to the actual numbers. Nationally, the median cost for in-home care is climbing, now sitting around $53,768 per year. That breaks down to about $4,481 a month for basic homemaker services and $4,576 for a home health aide.

On an hourly basis, you're looking at $23.50 to $24 per hour, and with rising demand, that number is projected to jump past $30 per hour by 2030.

Here in Texas, the rates are often a bit more manageable than the national average, but the same rules apply. For families in Willis and the greater Houston area, hourly rates will be in a similar ballpark, though they can shift based on local demand and the exact level of care needed.

The real challenge for families is balancing the hourly rate with the total number of hours their loved one needs. What starts as an affordable option for a few hours a week can quickly become a major financial strain when someone requires more than just part-time help.

From Hourly Rates to Monthly Totals

It’s easy to see how quickly the costs can add up. Let’s say a senior needs care for eight hours a day, five days a week. At an average of $25 per hour, that’s $1,000 per week. That simple math brings you to over $4,000 a month for just weekday, daytime help.

If your loved one needs support on weekends or overnight, that monthly total can easily climb past $7,000.

To help you get a clearer picture, we've put together a quick breakdown of national averages. This table shows what you might expect to pay for in-home care, from the hourly rate to the annual total.

National Average In-Home Care Cost Breakdown

| Care Type | Average Hourly Rate | Estimated Monthly Cost (44 hrs/week) | Estimated Annual Cost |

|---|---|---|---|

| Homemaker Services | $23.50 | $4,481 | $53,768 |

| Home Health Aide | $24.00 | $4,576 | $54,912 |

Source: Genworth Cost of Care Survey

As you can see, the costs are significant and underscore the need for careful financial planning. This pricing structure is why it's so important to understand the bigger picture of senior care.

In-home care offers the comfort of staying in a familiar place, but it’s just one piece of the puzzle. It’s helpful to see how these numbers stack up against other models, and you can learn more about the cost of independent living to get a different perspective. Ultimately, the goal is to find a solution that provides not just great care, but also financial predictability and a wonderful quality of life.

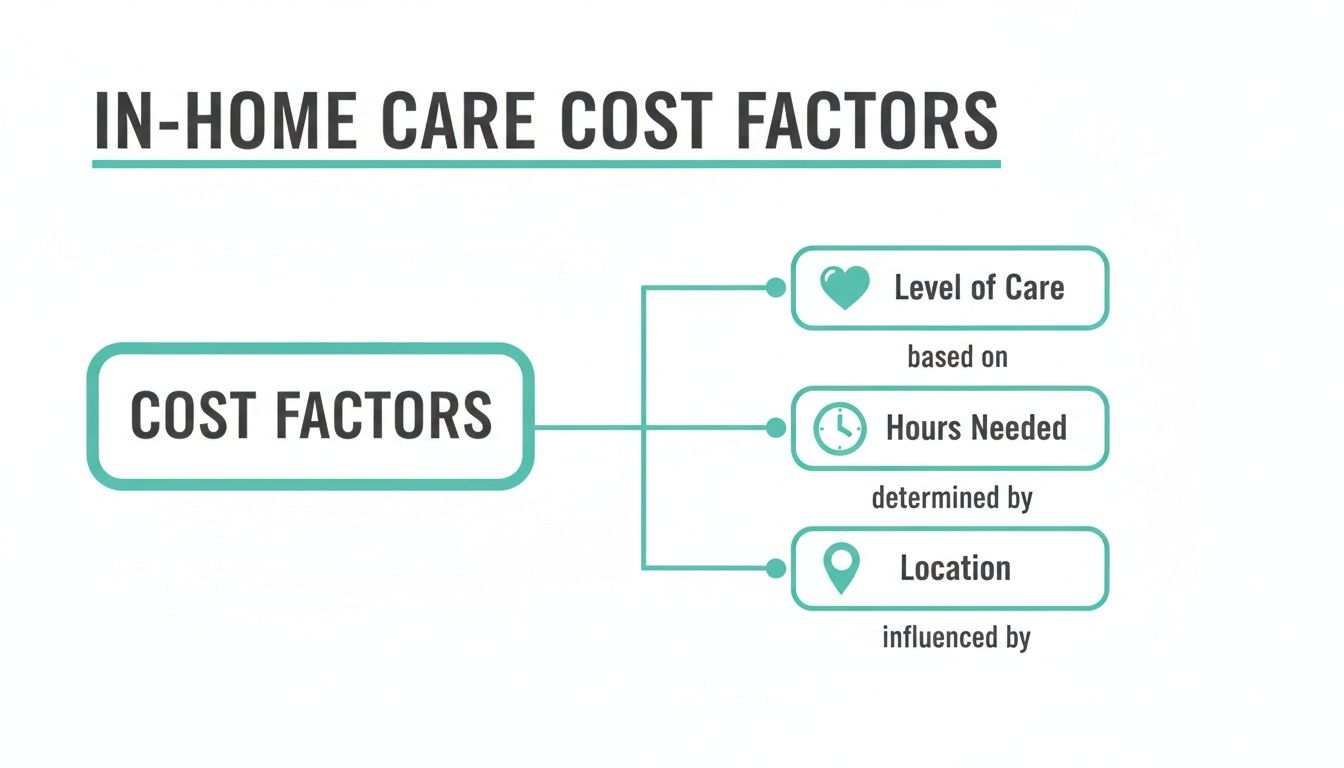

What Really Drives Your Final In-Home Care Cost?

Seeing an "average cost" for in-home care is a good place to start, but it's really just that—an average. The final price you'll actually pay can swing quite a bit because in-home care is never a one-size-fits-all solution. It's much more like building a custom service package; every piece you add or change adjusts the final price tag.

Several key variables come into play here. Getting a handle on them will help your family figure out exactly what you need and, just as importantly, how to budget for it. Let's break down the three biggest factors that will shape your total bill: the level of care required, the number of hours you need, and even your own zip code.

The Specific Level of Care Needed

The single biggest driver of your cost is the type of care your loved one needs. Not all help is created equal, and care agencies price their services based on the specific skills and qualifications a caregiver must have. This is why having a crystal-clear understanding of your family member's needs is so important.

Care generally falls into three main buckets, each with its own price point:

- Companion Care: This is the most basic and affordable level of care. It’s all about social interaction, light housekeeping, preparing meals, and running errands. It's a perfect fit for seniors who are still fairly independent but could use a hand staying engaged and managing their home.

- Personal Care Assistance: This level includes everything from companion care but adds hands-on support with Activities of Daily Living (ADLs). We're talking about direct help with bathing, dressing, grooming, and moving around safely. Since this requires more training and physical assistance, it comes at a higher hourly rate.

- Skilled Nursing Care: As the most expensive option, this care is provided by licensed medical professionals like Registered Nurses (RNs) or Licensed Practical Nurses (LPNs). This is for seniors who need medical help at home, such as wound care, injections, or managing complicated health conditions.

The difference in the hourly rate between a companion and a skilled nurse can be huge, often $15-$20 per hour or more.

Total Hours and Scheduling Demands

The next big piece of the puzzle is simple math: the more hours of care you need, the higher your weekly and monthly bills will be. A family that only needs 10 hours of companion care a week is looking at a very different budget than one that needs 40 hours of personal care.

But it's not just about the total number of hours. When you need that care also makes a big difference.

Many agencies charge a premium for services outside of standard business hours. You should expect to pay more for care provided at night, over the weekend, or on holidays, simply because caregiver pay scales are higher during those times.

For example, an hourly rate of $25 on a weekday afternoon could easily jump to $30-$35 for an overnight shift or on Christmas Day. It’s a critical detail to ask about when you're getting quotes from different providers.

Your Geographic Location

Finally, where you live plays a surprisingly big role in what you'll pay for in-home care. Just like with real estate, the cost of caregiving is tied directly to the local cost of living, regional wages, and the basic economics of supply and demand.

Typically, urban areas and their suburbs—like the greater Houston metro—have higher hourly rates than rural communities. This is because agencies face higher operating costs, and they have to offer higher wages to attract top-tier caregivers in a more competitive market. A caregiver in a major city might earn $25-$35 per hour, while a caregiver in a smaller, more remote town could be closer to $20-$25 per hour for the very same services.

By thinking through these three factors—the level of care, the hours needed, and your location—you can move beyond a vague national average and start building a much more realistic cost estimate for your family.

Comparing In-Home Care with Assisted Living

Deciding on the right care for a loved one often feels like standing at a financial crossroads. On one path, you have the perceived simplicity of in-home care. On the other, the all-encompassing support of an assisted living community. To make the best choice, you have to look past the sticker price and do a real side-by-side comparison.

Think of it this way: in-home care is like ordering from an à la carte menu. Every service, from a few hours of companionship to hands-on personal assistance, gets its own line item on the bill. This works well if your loved one only needs a little help, but as their needs grow, that bill can climb higher than you ever expected.

Assisted living, on the other hand, is more like an all-inclusive resort. A single, predictable monthly payment typically covers not just personal care but also housing, utilities, three meals a day, social events, and the peace of mind that comes with having staff available 24/7. When round-the-clock support becomes necessary, this model often makes more financial sense.

Uncovering the Hidden Costs of Aging at Home

When families start crunching the numbers for the average cost of in home care, they usually just focus on the caregiver's hourly rate. But that's only one piece of the puzzle. The true cost of staying at home runs much deeper, with plenty of "hidden" expenses that are usually already baked into an assisted living fee.

These extra costs can sneak up on you and really stretch a budget:

- Home Maintenance and Modifications: Think about ongoing repairs, yard work, and the cost of essential safety upgrades like installing grab bars, building a ramp, or remodeling a bathroom for a walk-in shower.

- Groceries and Meal Preparation: Even if a caregiver helps with cooking, the family is still on the hook for the grocery bills and the time it takes to plan meals.

- Rising Utility Bills: Having someone in the house around the clock means the lights, heating, and air conditioning are running more, leading to higher monthly bills.

- Transportation: Getting mom or dad to doctor's appointments, the pharmacy, or social outings becomes another expense and a logistical challenge to manage.

This diagram highlights the main drivers behind the direct costs you'll see from an in-home care agency.

As you can see, the direct cost is a moving target based on how much help is needed, for how many hours, and where you live—and that’s all before you even factor in the regular costs of running a household.

Cost and Service Showdown In-Home Care vs Assisted Living

To help visualize the difference, let’s put these two options head-to-head. This table breaks down what your money typically covers in each scenario, which can reveal a lot about the true value.

| Feature or Service | Full-Time In-Home Care | Assisted Living Community |

|---|---|---|

| Housing Costs | Not Included (Mortgage/Rent, Taxes, Insurance) | Included |

| Utilities | Not Included (Electricity, Water, Gas, Trash) | Included |

| Meals | Groceries Not Included (Cost of food + prep time) | Included (Typically 3 meals a day + snacks) |

| Home Maintenance | Not Included (Repairs, landscaping, updates) | Included |

| Social Activities | Limited (Companionship during shifts only) | Included (Daily scheduled events and activities) |

| 24/7 Staffing | Very Expensive (Requires multiple caregivers) | Included (Staff available around-the-clock) |

| Transportation | Not Included (Paid for separately) | Often Included (For appointments and outings) |

| Care Services | Billed Hourly (Costs rise with needs) | Included (Based on assessed level of care) |

Looking at it this way, it’s clear that the single monthly fee for assisted living bundles together a huge number of expenses that you'd be paying for separately—and often unpredictably—at home.

The Invaluable Price of Social Connection

Beyond dollars and cents, there's another cost to aging at home that’s harder to quantify but just as important: social isolation. Loneliness can take a serious toll on a senior's mental and physical health, contributing to depression, faster cognitive decline, and other major health problems.

While an in-home caregiver provides wonderful companionship, they are only there for their shift. They simply can't replace the built-in community of friends and neighbors that an assisted living environment provides. The spontaneous chats over coffee, shared laughter during a card game, and group outings are vital for well-being.

In an assisted living community, this social life is part of the daily routine, protecting residents from the risks of isolation and fostering a more vibrant, connected life. To see a full financial breakdown, you can dive deeper into assisted living costs in Texas and compare the numbers for yourself.

How to Pay for Senior Care in Texas

Once you have a clearer sense of the potential costs, the next question is always the same: How are we going to pay for this? It’s a question every family faces. Thankfully, there are several ways to fund senior care here in Texas, from personal savings and insurance to government programs.

Think of it like putting together a toolkit for a big project. You might find one tool that does the whole job, or you might need a combination of several to get the best result. Let’s walk through the most common funding sources so you can start building a financial plan that works for your family.

Using Private Funds and Assets

The most direct way to cover senior care costs is with private funds. This is the starting point for most families because it offers total flexibility—no applications, no waiting periods, and no eligibility rules to navigate.

These funds usually come from a handful of places:

- Savings and Investments: This is the money built up over a lifetime, including checking and savings accounts, stocks, bonds, and other investments.

- Retirement Accounts: Funds from an IRA, 401(k), or a pension plan are often used to cover the average cost of in home care or an assisted living community.

- Real Estate Assets: Selling the family home is a common strategy. It can convert a lifetime of equity into liquid funds ready to be used for long-term care.

A crucial first step for any family is to do a full financial inventory. Sit down together and get an honest, complete picture of all available assets. This will give you a realistic budget and empower you to make much clearer decisions.

Leveraging Long-Term Care Insurance

For families who planned ahead, a Long-Term Care (LTC) insurance policy can feel like a lifesaver. These policies are designed specifically to cover services like in-home care or assisted living when someone needs help with Activities of Daily Living (ADLs), like bathing or dressing.

But not all policies are created equal. You have to read the fine print to know what’s covered, the daily benefit amount, and the lifetime maximum. Some older policies might have quirky limitations or favor one type of care over another, so it’s important to confirm the policy covers the specific services your loved one needs right now.

Exploring Government and Veterans Programs

Beyond private savings and insurance, several government programs can offer major financial help. The eligibility requirements can be strict, but for families who qualify, these programs make a world of difference.

Medicare and Its Limitations

Here’s a common misconception we hear all the time: that Medicare pays for long-term care. The reality is, Medicare does not cover custodial care—the non-medical help with bathing, dressing, and other daily tasks. Medicare is for short-term, medically necessary skilled nursing care, usually right after a hospital stay. It’s not designed for ongoing senior living support.

Medicaid for Long-Term Care

Medicaid is a different story. This joint federal and state program does cover long-term care for people with limited income and assets. In Texas, the STAR+PLUS program helps eligible seniors get the care they need, including in an assisted living community. The rules can be pretty complex, so it’s often a good idea to chat with an elder law attorney or financial advisor to see if your family qualifies.

VA Benefits for Veterans

Veterans and their surviving spouses may be eligible for benefits through the Department of Veterans Affairs. A key program is the Aid and Attendance benefit, which is an extra pension payment that provides monthly funds to help pay for care. Our team has worked with many families to navigate these options. You can learn more in our guide on veterans benefits for assisted living.

Actionable Tips for Budgeting Senior Care Expenses

Figuring out how to manage the average cost of in home care takes more than just a calculator; it requires a clear financial game plan. Building a budget you can stick with isn't just about numbers. It's about creating a realistic strategy that ensures your loved one gets high-quality care without putting your family under financial stress.

The whole point is to feel confident and informed, making decisions that support your loved one’s well-being while giving everyone peace of mind.

It all starts with a thorough assessment of what care is truly needed. Before you can budget, you have to know exactly what services are essential versus what’s just nice to have. If you overestimate, you could end up paying for support that goes unused. Underestimate, and you might leave dangerous gaps in their safety and supervision.

By accurately defining your loved one’s daily requirements—from medication reminders and meal prep to mobility support—you can create a care plan that is both effective and cost-efficient, ensuring every dollar is spent wisely.

Build a Comprehensive Care Budget

Once you have a solid idea of the services needed, it's time to build a detailed budget. This goes way beyond just the caregiver’s hourly rate. A truly effective budget anticipates all the little expenses to prevent those "uh-oh" moments down the road.

Your financial plan should have a spot for:

- Direct Care Costs: This is the caregiver's hourly rate multiplied by the number of hours needed each week.

- Household Expenses: Factor in any potential increase in utilities, groceries, or household supplies.

- Medical Supplies: Think about costs for things like incontinence products, wound care supplies, or other necessities.

- Contingency Fund: It's smart to set aside a little extra for unexpected needs, like a temporary boost in care hours after a hospital stay.

Looking for ways to trim upfront costs? Exploring options like medical equipment rental services can be a savvy financial move. Renting items like a hospital bed or a walker offers flexibility and is often much more affordable than buying them outright.

Explore All Available Resources

No family should feel like they have to figure this all out alone. Many communities have programs and resources specifically designed to support seniors and their caregivers, which can seriously ease the financial strain.

Start by digging into local organizations that might offer a helping hand. This could include:

- Area Agency on Aging: These government-funded agencies are a fantastic resource for connecting seniors with local services, from meal delivery to transportation and even respite care grants.

- Disease-Specific Organizations: Groups like the Alzheimer's Association often have financial assistance programs or grants for families dealing with specific health conditions.

- Community and Faith-Based Groups: Don't overlook local churches and community centers. They frequently offer volunteer support or assistance programs for seniors in the neighborhood.

Short-term relief is also a huge part of a sustainable plan. For family caregivers who just need a break, understanding the respite care cost per day can help you plan for that essential rest without wrecking your budget. Having those open, honest family talks about money and who is doing what is the key to building a plan that works for everyone.

Putting Your Plan into Motion

Navigating the world of senior care can feel like a massive project, but you’ve just laid a solid foundation of knowledge. You've gone from wondering about the average cost of in-home care to understanding the real value of an assisted living community. Now, you’re ready to turn all those numbers and options into a real, personalized plan for your loved one.

The goal here isn't just about finding a place that meets their physical needs. It’s about finding a solution that brings them happiness, connection, and a genuine quality of life. Making this decision takes thoughtful conversations and a clear-eyed look at the financial side of things. You're now armed with the know-how on cost structures, hidden expenses to watch for, and how different types of care look at the whole picture of a senior’s well-being.

From Research to Reality

This is the perfect moment to take everything you've learned and see how it fits your family's unique situation. The best way to do that? See the options for yourself and get some professional insight that’s actually tailored to your loved one. Abstract ideas become much clearer when you can walk through a community, meet the people on the care team, and see residents enjoying their day.

This is where the numbers on a page truly come to life. A firsthand look helps you size up the environment, the quality of care, and the sense of community—factors that are every bit as important as the monthly price tag.

The next step isn’t about making a final decision today. It’s about gathering the final pieces of personalized information you need to make the right decision with confidence and peace of mind.

Your Invitation to Clarity

We believe every family deserves to feel certain and supported as they figure out the future. To help you take that next step, we invite you to connect with us in a way that feels right for you and your family. Getting that specific, personal information is the key to creating a care plan that actually works.

Here are two simple, no-pressure ways to get started:

- Schedule a Visit to Forest Cottage Senior Care: Come see our warm, homelike environment for yourself. A tour is the best way to get a true feel for our community and ask any questions you have on your mind.

- Request a Personalized Care Assessment: Let our experienced team help you understand your loved one's specific care needs. This assessment gives you a clear picture of the support level they require and what that looks like financially, giving you a concrete budget to work with.

Taking one of these steps will provide the final, crucial details you need. It replaces uncertainty with a clear, actionable path forward, ensuring your loved one receives the wonderful care they deserve.

Answering Your Top Questions About In-Home Care Costs

When you start digging into the finances of senior care, a lot of questions pop up. It’s completely normal. To help you get some clarity, we've put together answers to the most common things families ask when trying to figure out the average cost of in home care. Think of this as a quick-start guide to give you the confidence to take the next step.

Does Medicare Pay For 24/7 In-Home Care?

This is probably the biggest point of confusion for families, and the answer is simple: No, Medicare does not pay for 24/7 in-home care. Medicare is set up for short-term, skilled medical care after something like a hospital stay—not for long-term personal assistance.

Custodial care, which is help with daily life like bathing, getting dressed, and making meals, isn't covered. For that kind of ongoing, non-medical support, families typically rely on private funds, long-term care insurance, or Medicaid if they qualify.

Is In-Home Care Cheaper In Smaller Texas Towns?

Generally, yes. The cost for in-home care tends to be lower in smaller towns and more rural parts of Texas compared to big cities like Houston or Dallas. It really just comes down to the local cost of living and what the average wages are in that specific area.

You might find hourly rates in a smaller Texas town to be $3-$5 less than in a big city. The trade-off, however, is that it can sometimes be a bit harder to find available, qualified caregivers in less populated areas.

What Is The Real Difference Between A Home Health Aide And A Homemaker?

People sometimes use these terms as if they mean the same thing, but their roles—and their costs—are quite different. Knowing which one you need is key to getting the right support without paying for services you don't.

- Homemaker Services: This role is all about managing the household and providing companionship. Think light housekeeping, cooking, running to the grocery store, and just being there for conversation and social engagement.

- Home Health Aide (HHA): An HHA can do everything a homemaker does, but they also have training to provide hands-on personal care. This means they can directly help with things like bathing, dressing, grooming, and moving around safely.

Because HHAs have that extra level of training, their hourly rate is usually a few dollars more.

Can We Hire A Caregiver Directly To Save Money?

On the surface, hiring a caregiver on your own (sometimes called a "private hire") looks like a great way to save money by cutting out agency fees. But this path comes with a lot of responsibility and potential costs you might not see at first.

When you hire directly, you’re not just hiring help—you’re becoming an employer. That means you’re on the hook for managing payroll, withholding taxes, getting liability insurance, and running background checks. You're also the one who has to scramble to find a replacement if your caregiver calls in sick or takes a vacation. An agency handles all that behind-the-scenes work, which gives you a much more reliable and legally sound care solution.

Working through these details is a big part of planning for your loved one’s future. At Forest Cottage Senior Care, we believe in being completely transparent to help you make the best decision for your family. Schedule a visit today to learn more about our simple, all-inclusive pricing.